With current growth trends changing the very structure of the global pharmaceutical market, pharma business consultancy IMS warns that the sector must rethink its future business models. Susan Birks reports

A revised forecast released by business intelligence and strategic consulting service IMS suggests global pharma growth in major developed markets will slow further than previously predicted in 2009. Already facing the lowest growth prospects ever, the economic downturn has led IMS to drop its 2009 forecast by a further couple of per cent and it expects all of the mature markets to be in recession this year.

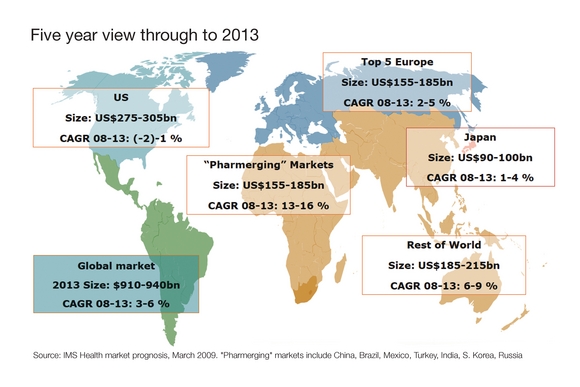

In 2010, IMS forecasts further contraction or flat results in the top five traditional markets (US, Japan, Canada, Germany, France) with only the emerging markets likely to present good future growth. The US market is forecast to have a negative growth rate of -2 to -1% in 2009. The top five European markets are forecast to see a meagre 2-3% growth and Japan only 4-5% growth.

Looking ahead to 2013, the US market is predicted to remain flat; Europe's growth is forecast to be anywhere between 3-5% and Japan's 1-4%, while the emerging markets continue to make double figures (see figure 1).

The emerging pharmaceutical markets, coined by some as pharmerging. markets - Russia, Brazil, China, India, South Korea, Turkey and Mexico - are set to see better growth than the traditional markets, but at a lower rate than in recent years.

What the figures show is that the mature pharma sectors are being hit not only by the difficult economic climate, but also by long-term trends that are forcing rapid change in the way pharmaceutical companies do business.

"In such challenging times, the pharma sector needs to find new value propositions and new business models if it is to see future growth," says Robert Arnold, IMS vice president of product & portfolio strategy.

New decision makers

Pharmaceutical companies have traditionally targeted their marketing and sales efforts towards doctors or physicians but increasingly the decision makers are the large healthcare providers ("the payers"), whose decisions are based on curbing drug spend and introducing wider use of generics.

Sati Sian, general manager of commercial effectiveness at IMS, highlights that the industry is also facing tighter controls over physician prescribing decisions. Stricter controls now exist on access to physicians and on commercial practices such as the giving of promotional gifts, he said.

As a result, multinationals are already seeing rapidly decreasing productivity from their massive sales forces and, according to Sian, they need to reallocate nearly US$15bn in promotional spend that currently provides no return on their investment. "They need to rethink the commercial model to take into account the new stakeholders," he says.

Companies need to "look at who their customer really is", says Arnold, "and to make their value propositions meet those things that are currently high on the list of what "the payers" want to spend money on".

This re-tuning of commercial activities to the needs of "the payers" will for many companies require a reorganisation of the workforce with the implementation of integrated teams who can talk to "payers".

To make matters worse, "the payers" are increasingly focused on patient outcomes, more so than in the past, so companies need to create products that are "synergistic with outcomes".

"They increasingly want metrics and the [pharma industry's] model is not set up to do this", says Arnold.

Risk sharing

Companies need to offer what he called more integrated value propositions, sharing the risk of the uncertainty in efficacy, and hence the cost incurred by non-responsive patients.

The idea of enabling the payer to pay only for the patients for whom the product works sounds revolutionary but it is already happening, says Sian. He cites an example in which J&J has devised a risk-sharing deal that offered an efficacy guarantee to the NHS for its Velcade (bortezomib) for injection.

Patients showing minimal or no response would be taken off Velcade with costs refunded by J&J. Patients showing a full or partial response to the drug after a maximum of four cycles of treatment would be kept on Velcade, with the treatment funded by NHS Vision.

GSK in Iowa, US, is following a similar proposition for its treatment for osteoporosis by offering to cover all the treatment costs for bone fractures for those on the therapy.

Future business needs to create similar win-win propositions with the payers that will overcome market access barriers.

Personalised medicine

But for some in the industry even this change will not be enough. According to Arnold, some companies are already "talking about de-emphasising traditional pharma from their portfolio". An alternative area that he suggests companies should look at for future development is regenerative medicine - a sphere in which the industry has a good basis to start "as it already understands the needs of the clinic", he says. He also suggests companies should be investing in new technology for personalised medicine, and in biotech, as the economic downturn has created "a window in which to shop for biotech companies" while prices are at an all time low.

More importantly, drug companies need to focus their agendas on the emerging markets where future growth is most promising.

A new world order is already emerging with China and India providing huge new markets. Despite the current economic difficulties, the Chinese government has committed to spending $23bn on its healthcare market and IMS predicts that by 2013 China will become a top 3 market. India, meanwhile, is investing to become the world's largest biopharma market.

The short term forecast for all the emerging markets is favourable and IMS is confident that growth "will remain strong and [the markets] will almost double in size in the next five years". It predicts that out of the seven emerging markets, China, India, Turkey and Russia will see double-digit growth in the next five years.

Despite the huge coverage in the press about the rise of markets in the East, IMS believes Western pharmaceutical companies have been slow to maximise their value.

"Many companies have failed to capitalise on the opportunity in the pharmerging markets," says David Campbell, IMS senior principal, PPS. He points out that only one-third of the 420 NCEs launched since 1997 have reached these markets.

Only now is the sector starting to see some urgency in the need to invest in emerging markets. Sanofi aventis and GSK are among those to have already invested in acquisitions and, according to IMS, more than 70% of sanofi aventis" pharmaceutical growth in 2008 came from emerging markets.

Unique market conditions

The challenge companies face is that each of the emerging markets is unique and requires different modes of access: India is dominated by the local generics market, while Turkey's market is mainly one of branded medicines and China is heavily influenced by traditional medicines.

"Traditionally multinationals have taken business models from mature markets and dropped them into emerging markets and that doesn't work," says Campbell.

The industry needs to prioritise these markets and build new models for them but to do this they will also need people who know how the local markets work, adds Campbell. "The key to success across the pharmerging market is local adaptability. Not only do companies need to align their portfolio with the high growth opportunities, but they also need to match local demand with value propositions and build the right sales and distribution models to get them to customers."

Clearly, staying with the old business model is not an option, and even when the current recession is over, the pharmaceutical market of the future is going to look very different from what we have now.